Commuters of Bengaluru have reason to cheer. The Bengaluru Metropolitan Transport Corporation (BMTC) has announced an upgrade to its ticketing system to enable payments using the National Common Mobility Card (NCMC) that has been a demand from the public since its younger sibling, the Bengaluru Metro Rail Corporation Limited (BMRCL) enabled it in 2022-2023.

In a report titledTap, scan, go: BMTC launches smart ticketing across fleet in the Bangalore Mirror, it has been reported that digital payments made up close to 20 per cent of the corporation’s daily ticket revenue, driven by its static QR Code payments system. Interestingly, in another report titledPayment failed, Bangalore Mirror reports that UPI is not a preferred option in sub-urban, semi-urban and rural parts of the city due to connectivity issues leading to people preferring to pay cash.

As per the first report, BMTC is looking at getting Android-based ‘Smart’ Electronic Ticketing Machines (ETMs) which is kind of suspicious, since the existing machines in use are Android-powered Pine Labs machines. However, a contradiction is observed in the next paragraph, where it says that the ETMs are already in use. The demand for NCMC integration however is due to the fact that BMRCL is already using them and keeping this in mind, it would be fair to assume that BMTC won’t make the mistake of going for an ‘exclusive NCMC‘.

The ticketing upgrade will also upgrade the BMTC’s vehicle tracking capabilities, building on its Automatic Vehicle Location System (AVLS). While not reported, integration into mapping platforms using the General Transit Feed Specification (GTFS) is also a likely outcome.

Another change expected as part of the upgrade is the introduction of dynamic QR codes. Interestingly, in an report published by The Hindu, there was a demand for the existing static QR code system to continue, but the demand was for conductors to carry the QR Code as a badge as it was difficult to scan the QR Codes on the walls on the bus. In all fairness, the existing setup works perfectly and both, asking the conductor to carry it or a Dynamic QR code will merely make things more difficult.

Let us see what happens. Interestingly, BMTC in 2017 had partnered up with Axis Bank to establish an EMV open-loop payment system, nearly two years before the NPCI launched the NCMC framework It was quickly phased out a year later.. Among other factors, it was reported by Christin Mathew Philip of MoneyControl in 2024, that BMTC with a daily ridership of 38 lakh was not keen on accepting the Namma Metro NCMC because BMRCL had a ridership of 7-8 lakh. A rather deluded argument, if you ask me, but I sincerely hope that this does not give the administration any ideas to go in for an exclusive NCMC. Karnataka was the after all the first state in India to introduce electronic ticketing on 15 August 2004.

Featured Image: Conductor selling tickets with a Ticket Machine (Image animated using Grok/xAI)

We’ve always associated buses of the Brihanmumbai Electricity Supply and Transport (BEST) undertaking with red but did you know that there was a point when that was not the case? Over the years, we’ve seen some exceptions to the rule, such as the vestibule fleet that was yellow in colour, much like the current Tejaswini fleet for women. Similarly, the JCBL Cerita (erroneously referred to as Kinglong) was purple in colour (hence I referred to them as Purple Faeries) and the Tata Starbus Hybrid fleet was silver in colour. Of the six Volvo buses in its fleet, a few were orange while the rest were red, although only the front of the bus reflected this, given that advertising covered the sides as part of the acquisition deal. However, barring these, the fleet has pretty much been red. The same applied to trams too. However, there was one period when the buses were painted a different colour.

India was an active participant in both World War I and World War II as a part of the British Empire. As a result, Indian cities, especially the larger ones were at high risk of being attacked by the enemies. While electricity was yet to reach all parts of the city, public areas were often illuminated and buses and trams, being a bright-red colour were at constant risk of being targeted.

BEST’s buses in the military green livery from 1941 to 1945. Image courtesy BEST

Thanks to Shubham Padave, Yatin Pimpale for the information. Thanks to BEST for the image.

Featured Image: An AI-generated rendition of a BEST bus in military olive green; generated using Dall-E 3 on Bing.

In a move aimed to give commuters slight relief, buses of the Brihanmumbai Electricity Supply and Transport (BEST) undertaking can now be tracked live on Google Maps. The service was launched by Maharashtra Chief Minister Devendra Fadnavis.

BEST will be using the General Transit Feed Specification (GTFS) format developed by Google, which is an open-source format used for pulic transport schedules. Data will be available in Marathi, Hindi and English. BEST has been working with Google for the last two months and the mechanism is also integrated with timings of both Indian Railways and Mumbai Metro.

Maharashtra CM Devendra Fadnavis with the Google team and DyCM Eknath Shinde (Pic tweeted by BEST on Twitter)

While this is overall a good move, there is a slight downside to it. Given the present circumstances and what happened over the last few years, it is imperative that local platforms are developed as alternatives to Google.

Readers may remember that under the Joe Biden administration, the United States of American imposed sanctions on Russia, leading to huge queues on the Moscow Metro when Google Pay and Apple Pay refused to work. Of course, Russia quickly developed its own ‘Faster Payments System’, based on the National Payment Card, but the damage was done. While India has ensured that payments won’t fail with the domestically developed RuPay-based NCMC, data sovereignty remains a critical factor, especially when it comes to maps and navigation. Do remember, in 1999, during the Kargil War, the United States under Bill Clinton refused to allow us to use GPS. Eventually, India developed its own range of navigation systems, from ISRO’s Bhuvan, to the Indian Regional Navigation Satellite System (IRNSS), also known as NavIC. We have domestic map suppliers such as MapMyIndia’s Mappls and Ola’s Krutim-powered maps.

It’s official. The Brihanmumbai Electricity Supply and Transport (BEST) undertaking is finally revising its fare after slightly over five years. And while most media publications are describing it as a ‘sharp’ or ‘significant hike’ it is isn’t all too bad. The new fare structure has got approval from the Municipal Corporation of Greater Mumbai (MCGM) and is currently awaiting approval from the Mumbai Metropolitan Region Transport Authority (MMRTA). Officials say that the fare hike was unavoidable as the incumbent fare structure was too low and the undertaking was bleeding revenue. Prior to the fare reduction, the minimum fare in BEST’s non-AC buses was ₹8.

As per reports, the minimum fare would be doubled, essentially reaching the next fare stage of ₹10 for non-AC and ₹12 for AC buses.

The new fare structure is given below

Fare Stage

Non AC Fare

AC Fare

0-5km

₹10

₹12

5-10km

₹15

₹20

10-15km

₹20

₹30

15-20km

₹30

₹35

20-25km

₹35

₹40

The rates for weekly and monthly passes have also been raised. There will also be additional surcharges for leaving the limits of the municipal corporation and crossing toll plazas.

Featured Image: Conductor selling tickets with a Ticket Machine (Image animated using ChatGPT/OpenAI)

In what can only be termed as good news, Mahaarashtra Chief Minister, Devendra Fadnavis has given a nod for the Brihanmumbai Electricity Supply and Transport Undertaking (BEST) to redevelop three bus depots – Bandra, Deonar and Dindoshi – as part of a plan for the undertaking to generate additional revenue.

BEST has in the past redeveloped its existing land assets as part of plans to monetise them. Starting over 20 years ago, the Seven Bungalows (Saat Bangla) bus station was redeveloped as the ill-fated G7 shopping complex. A similar project began at the Marol Maroshi bus station. The once-dreaded Kurla depot which had been damaged in the 2005 floods was eventually redeveloped by Kanakia as Kanakia Zillion along with the Mahim and Versova-Yari Road (Vesave-Yari Road) bus stations as Kanakia Miami and Kanakia Hollywood respectively.

BEST officials also urged Fadnavis for a fare hike, but the Chief Minister asked them to put forth a formal proposal first.

The Bandra depot –which once also was home to a slaughterhouse in the vicinity – has had large amounts of land encroached upon. The Municipal Corporation of Greater Mumbai (MCGM) – BEST’s parent body – is simultaneously building an access road behind the depot to connect it to the Western Express Highway.

BEST’s redevelopment plans, however, have not been without controversy. At the site of the Mahim bus station, 1,000sqft of land was leased out to Fortpoint Automotive in 1993 and subsequently extended till 2018. In 2007, Parsvnath Developers was given the tender to remodel and redevelop the 2 acre plot at a cost of ₹22 crore. In 2010, Kanakia took over the project. In 2015, BEST terminated its lease with Fortpoint, which then went to court before getting a favourable ruling in 2017. Later that year, the MCGM asked for BEST to surrender the land that had earlier been leased out to Fortpoint as setback land – a prerequisite for granting of completion and occupation certificates for the tower coming up atop the bus station. At the site of the Marol Maroshi bus station, BEST had given the tender to KSL and Industries in 2008, who in turn subcontracted it to Dhruvi Properties, allegedly circumventing procedure. The matter came to light when property buyers approached the Maharashtra Real Estate Regulatory Authority (MahaRERA). Interestingly, one name that popped up was that of BEST’s former General Manager, Uttam Khobragade. To read more about his contributions to BEST, do read: The ‘BEST’ scamster Indians should know about – Congress and the Khobragades have a lot to explain.

Fadnavis urged officials to find feasible ways to increase the fleet strength of the undertaking, which has been dwindling over the last few years. It currently operates a mere 2,783 buses including both buses owned by the undertaking and on wet lease, down from 3,228 in 2023 and 4,608 in 2011. He advised officials to look for funds under the Centre’s National Clean Air Policy (NCAP). He also urged the MCGM to allocate at least 3% of its budget to BEST. He also said that BEST would soon sign an MoU with Google to give commuters real time updates for buses.

One untapped market for the National Common Mobility Card (NCMC) is Indian Railways, especially for suburban rail services.

Currently, buying tickets on Indian Railways happens across three forms – buying directly at the counter, paid with cash of UPI, buying it on one’s phone using the UTS app or buying it at an automated ticket vending machine (ATVM) using either a prepaid smart card or UPI. In the earlier days, IR also sold coupon booklets of coupons with varying denominations that the commuter would then validate using a coupon validating machine (CVM) which essentially stamped the date and time on the coupon. This was done away as the Railways wanted the entire system to be computerised.

The existing system has a lot of issues, but implementing the NCMC shouldn’t be difficult.

For starters, it must be noted that unlike its newer counterparts – metro rail – suburban rail predominantly operates using a proof-of-payment system. You buy the ticket before boarding. The system is not too different from buses – where NCMC is already operational across many cities – with the only difference being that in the bus, the ticket is bought on-board and for the train, it is off-board.

The simplest method for this would be to allow passengers to walk up to the existing ATVM, place their NCMC on the card slot and buy the ticket. There are two types of ATVMs, one which accepts UPI or the existing smart card and one – called the Cash/Smart Card Operated Ticketing Kiosk (which for some reason is abbreviated as CoTVM – which can accept coins and banknotes as well. Only the cash input system is different, otherwise they are identical in every other way. The booking interface itself is quite easy. The machine allows you to book tickets with the aforementioned smart card, recharge the card (with UPI or cash, depending on which machine it is), print a ticket booked with the UTS app (by entering the mobile number and four-digit ticket number) and platform tickets. Beyond this, for UPI transactions, you can book with three options. Fast booking allows you to book from a preselected list of top stations, book using the map allows you to select the stations from a map and the third option, all other stations, allows you to type the station name or code and book the ticket. For smart card users, for the entire process, the card is placed in a tray below the screen. Tell me why this system should not be accepting the NCMC.

The second option would be to allow NCMC cardholders to tap-in and tap-out, akin to an automated fare system. This system has partly been tried out in India before, nearly two decades ago, with the Go Mumbai smart card that was operational in Mumbai’s suburban trains and BEST buses nearly two decades ago. However, the Go Mumbai Card operated on a fixed-fare basis, meaning, it could only be used for a specific fare stage, both for buses and trains.

To explain, I had gone to apply for one in 2006-2007. The person behind the counter at the JVPD bus station asked me which bus I took and what the fare was. Now this was a problem. By default, I took 56 from Four Bungalows Market to Santacruz Post Office for ₹5. However, if a 38 came, I would board that for ₹7. If neither came, I’d walk to ESIC Nagar and take a 79, 33 or 241 to Santacruz Station for ₹5, a 355Ltd to Santacruz Post Office for ₹6, 200 or 222 to Santacruz Post Office for ₹7. Essentially, I had two parallel routes, each with different fares and stages. Plus, on weekends, I used to go for classes which meant I’d pay ₹3 in a 56 or a 221, but one was from Four Bungalows Market and the other from Juhu Versova Link Road. Pretty complicated? Not really. The card worked on only one route on one stage. The conductor merely checked whether it was valid for that stage or not. The same happened with the train. Passengers bought it for a certain trip, between Station A and Station B, for a particular class. They’d tap it at the validating machine at both stations.

Replicating this with the NCMC should not be difficult. However, due to volume of passengers – Mumbai alone has a daily ridership of 62 lakh – implementing an absolute automatic fare system with turnstiles would be difficult. Here, having NCMC holders swipe in and swipe out and different stations would require them to do it at both stations. Ticket checkers are usually present in high-traffic stations and can be given a machine locked into that station. Presenting the NCMC there should ideally validate the swipe out so that passengers don’t have to then swipe out. Not swiping in and popping up on the machine can automatically deduct the fare from the card. However, dispute resolution mechanisms should be put in place in case the entry swipe wasn’t captured due to any technical fault.

However, the situation gets complicated due to different classes. Suburban rail in India has two classes by default – second and first class – with Mumbai and now Chennai also having a third one in the form of air-conditioned trains. The only incumbent rapid transit system with multiple classes in India is the NCRTC’s Namo Bharat RapidX train where premium class passengers cross two turnstiles, one at the concourse level to enter the ticketed area and once again at the platform level to access the premium lounge and coach. This may not work well on suburban trains simple because there are multiple first class coaches spread across the train and the issue will be further compounded when trains of different lengths arrive on the platform. A secondary solution can be to set up a second machine inside the compartment itself or mounted on the exterior wall that can be tapped on entry. But given the crowds, how practical this can be, remains to be seen. If such a system is established, then it would require a separate machine for purchasing platform tickets as well. Nearly two decades ago, South Western Railway had installed ticket vending machines at the KSR Bengaluru City railway station to sell platform tickets. These German machines, built by Hectronic were coin operated, but fell into disuse when platform ticket fares went up and the coin size the machine was designed for was no longer being minted. An NCMC-enabled version is simple. Tap it and it just prints a ticket. Tap it mulitple times for multiple tickets.

However, since the NCMC in its current form doesn’t seem to support passes, season tickets would become problematic.

Allowing for the NCMC to be used to buy tickets using the ATVM, seems to be the best way to get the Indian Railways on to the NCMC bandwagon.

Featured Image: A generic NCMC being held up against a Western Railways AC Local in Mumbai (Image generated via Sora/ChatGPT/OpenAI)

So, one interesting debate that has happened recently is the question of which is better on a bus – the Unified Payments Interface (UPI) or the National Common Mobility Card (NCMC).

Interestingly, a lot of people (who don’t seem to use public transport, as evident from their tone) believe that UPI is a far superior option. In fact, in one discussion on Twitter (I refuse to call it X), I was told by a self-described techbro that UPI is convenient as people have their phones handy and use UPI to buy chai and flowers, and specified that taking out the wallet to take out an additional card in a crowded bus was a burden and not advisable. Sure, but typing out my UPI PIN in front of 30 other people is kosher. Or making others wait while you enter your pin, and the transaction takes its time is absolutely alright.

But let us not digress. We’re now solely looking at which is better, NCMC or UPI. UPI is a great option if either you or the conductor does not have change (or cash for that matter) and you don’t have an NCMC as well. Conversely, if everyone is accepting NCMC and you have one, you can use it here too, right?

Now, in order to test this hypothesis (if you can call it one that is), I used both NCMC and UPI to buy tickets. I used the NCMC at two places: BEST in Mumbai and MTC in Chennai and UPI at two places: BMTC in Bengaluru and MTC in Chennai.

Let’s start with NCMC. It’s easy to use. In most cases, you hand over the card, say NCMC or Metro Card and that gets the job done. With BEST, I was unsure if my RBL NCMC would work, the conductor reassured me by saying that “he’d make sure it worked”, while with MTC, I have told most conductors that it is a valid card and that I have used it before but eventually they accept it. The whole process is quick, takes about five seconds and is often faster than cash because the conductor does not have to count for change. There’s really not much to say because it is a fairly simple and straightforward process. The only time consuming part is to convince the conductor that the card is valid. This has happened with my RBL, Ongo and Airtel cards.

An NCMC ticket issued by BEST (Pic: BESTpedia)

The only issue is that the card needs to be topped up after 20 or so transactions (some lame protection feature apparently) and this happened with me recently. The conductor topped my card up for ₹0. Since my phone supports NFC, I figure the easiest workaround for this is to top up the card for smaller amounts, rather than loading it up for the entire ₹2000 that the card can support.

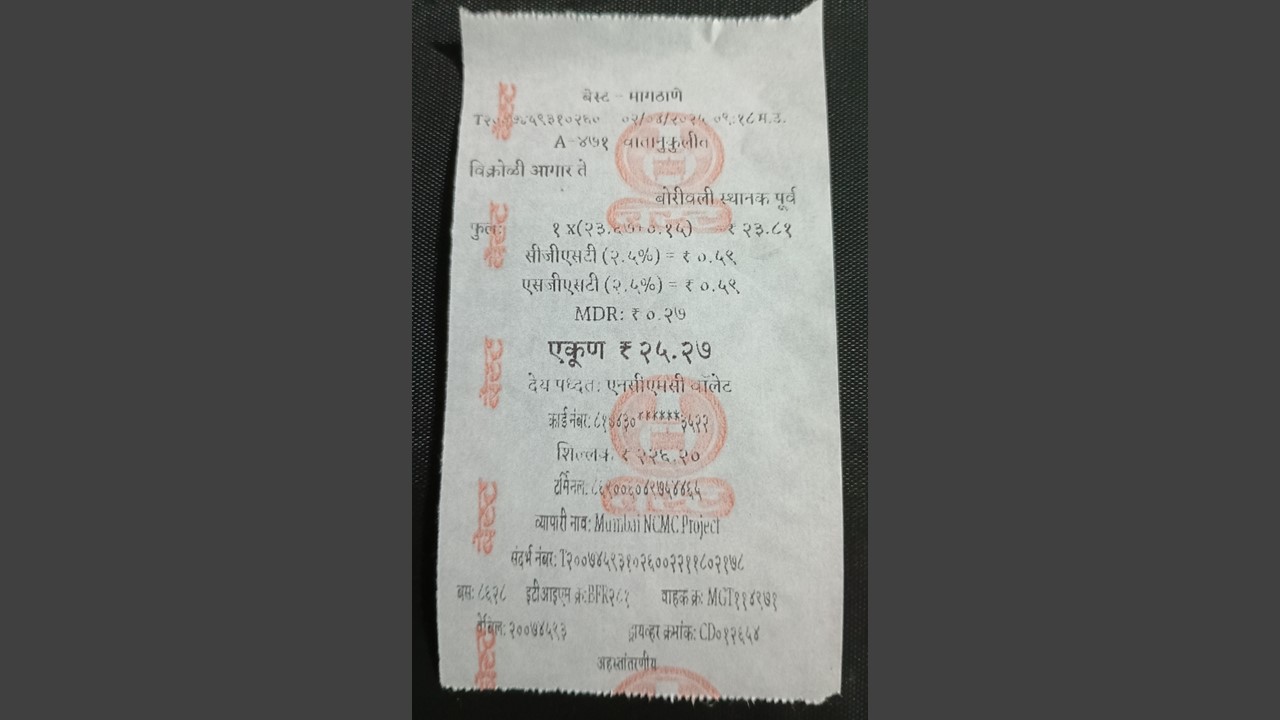

Another issue is that of the Merchant Discount Rate (MDR). Some transport companies charge extra for this, such as BEST, while most absorb it into their fares. Here is a quick breakdown of BEST’s MDR charges for different fare stages (Regular/Limited/Express/AC): ₹5 – 6 paise ₹10 – 11 Paise ₹15 – 16 paise ₹20- 22 paise ₹6- 7 paise ₹13- 14 paise ₹19- 21 paise ₹25- 27 paise

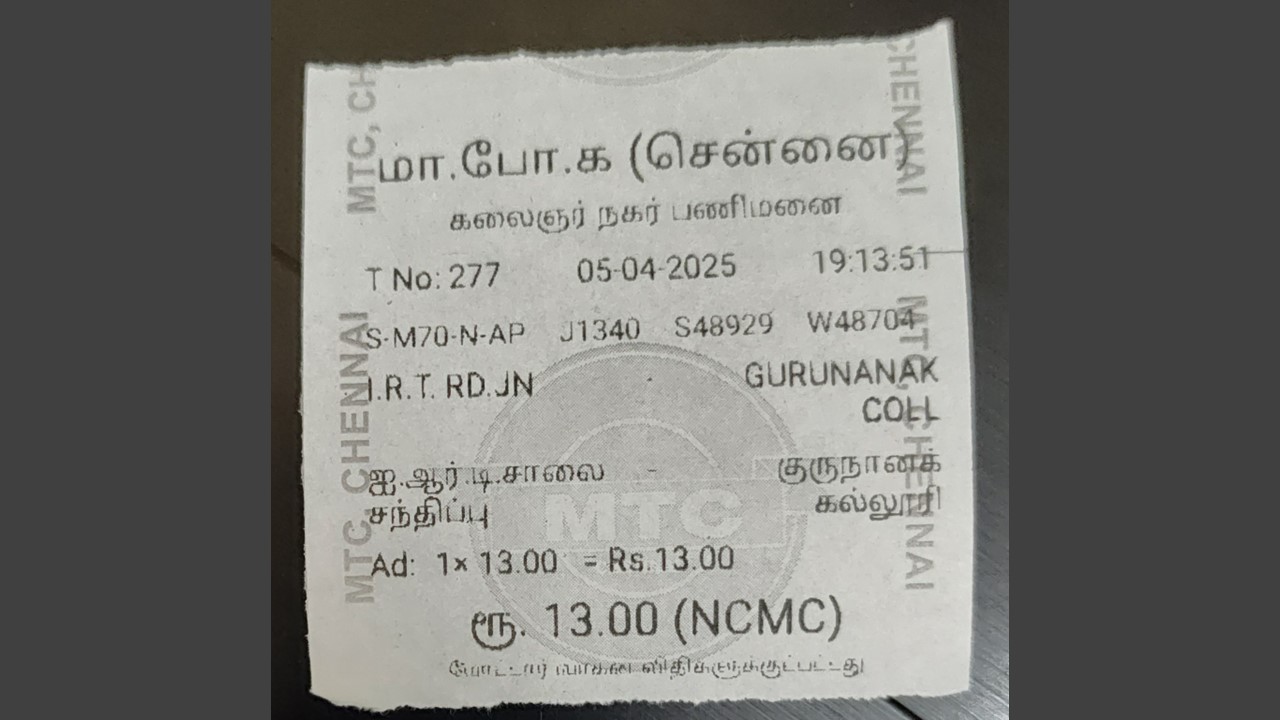

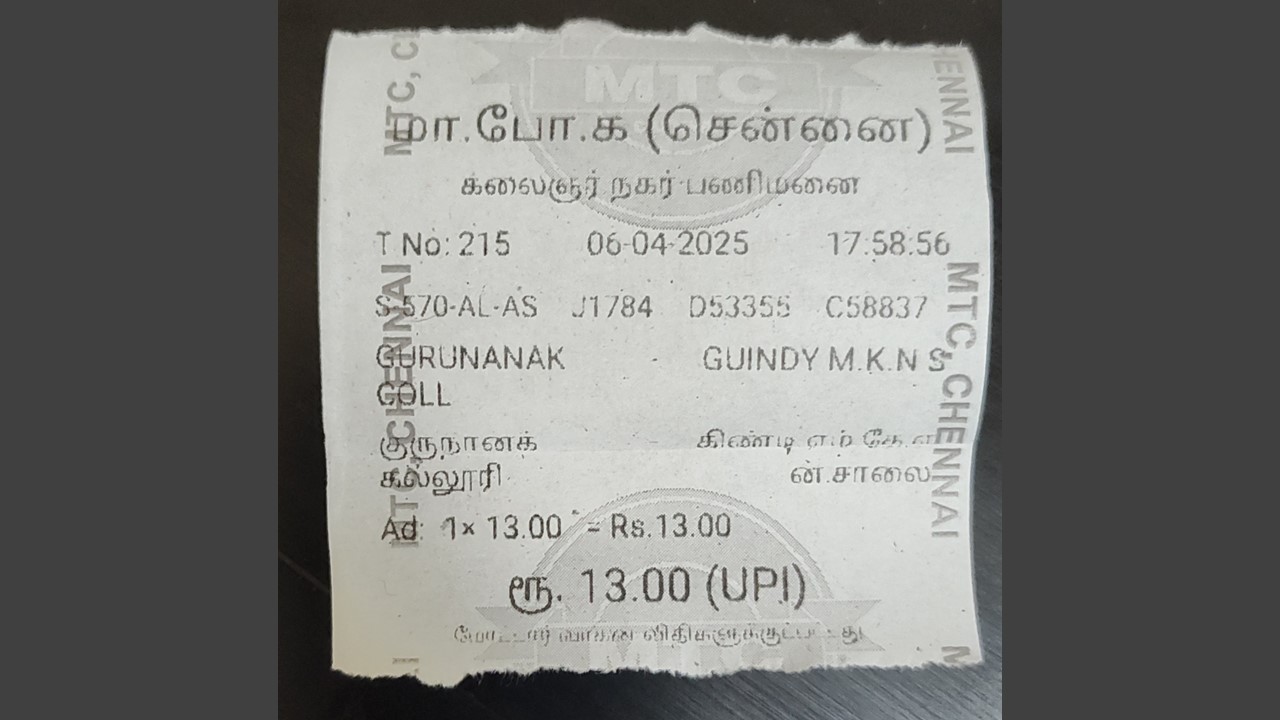

An NCMC ticket issued by MTC (Pic: BESTpedia)

Now, coming to UPI. This is where things get interesting. I’ve used two different methods of paying via UPI. One is with a static QR Code on BMTC and the other is with a dynamic QR Code on MTC.

A UPI ticket issued by BMTC (Pic: BESTpedia)

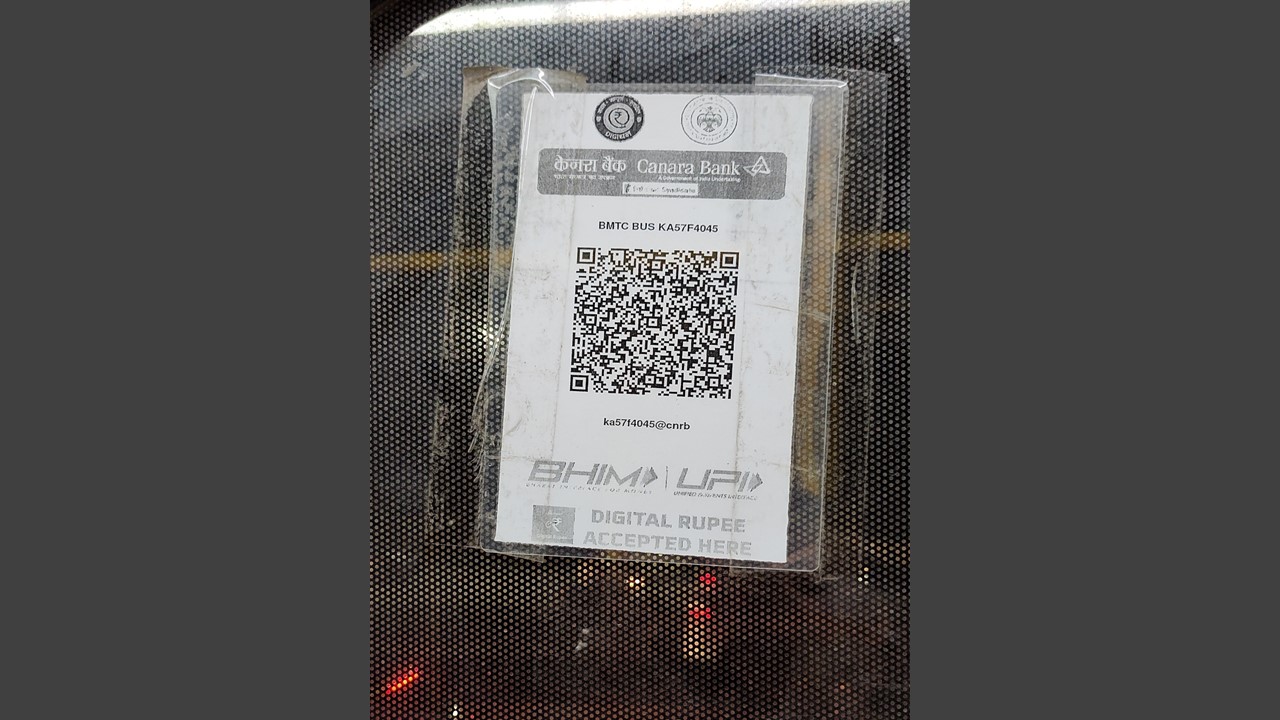

Now, the BMTC model is very simple. BMTC began accepting UPI payments in 2020, during the lockdown to reduce contact between passengers and commuters. BMTC Finally Starts Cashless Ticketing, Uses UPI-Based QR Codes For Transactions Each bus has its own virtual payment address (VPA, often erroneously referred to as UPI ID) which is the bus’ registration number attached to a Canara Bank Account; Eg: KA57Fxxxx@cnrb. QR Codes for the same are pasted in different parts of the bus, and in some cases, they are also present in the transparent grab handles of the bus.

BMTC QR Code Sticker on the bus (Pic: BESTpedia)

In my case, neither the conductor, nor I had change, so he told me to scan the QR Code and pay. I did, showed him the successful transaction screen and he issued the ticket. This method is extremely popular with passengers using it for as low as ₹5. However, there seems to be no way for the conductor to validate the payment. However, since the ticket machine being used is a standard Pine Labs point-of-sale device, maybe it appears there. This being said, it is high time that BMTC and Canara Bank adopted the NCMC. The process is reasonably fast, although it depends on how fast your internet connection is and multiple people can pay simultaneously making it relatively faster than dynamic QR Codes.

A UPI ticket issued by MTC (Pic: BESTpedia)

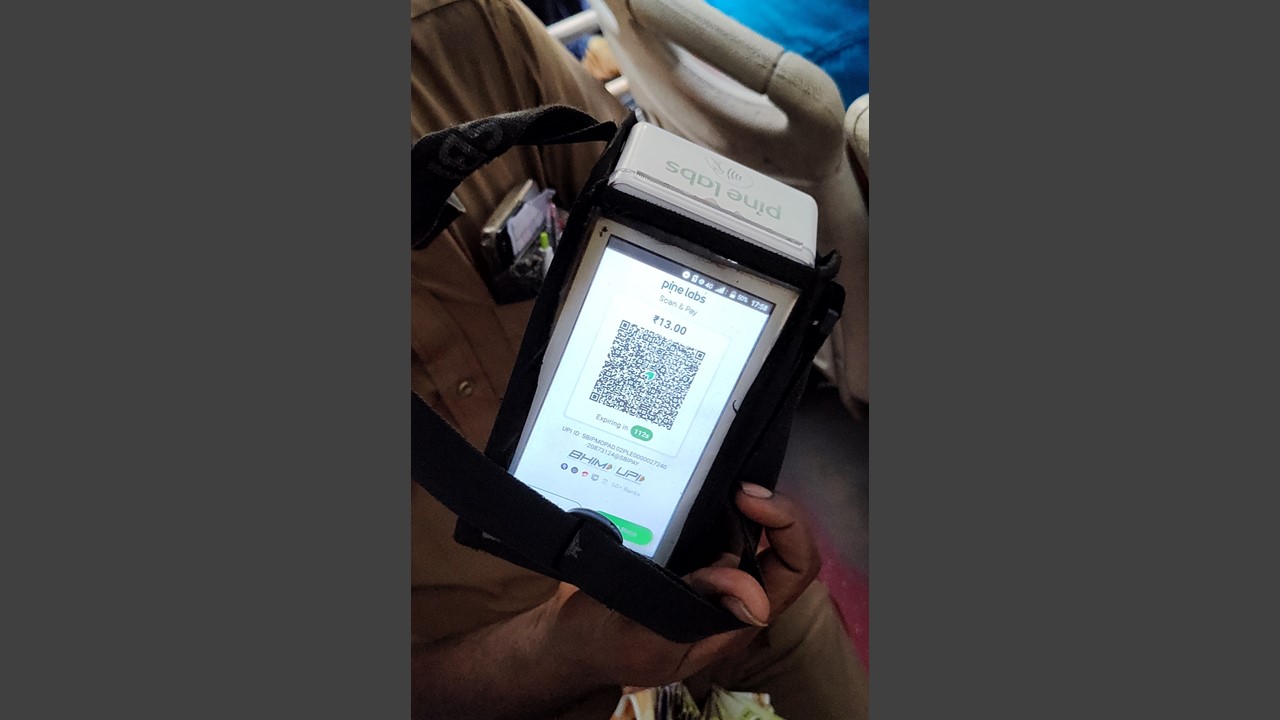

Now, coming to the Dynamic QR Code. Here, the conductor has four options on the ETM – Card, UPI, NCMC and Cash. When the conductor selects UPI, it generates a dynamic code that one scans and makes the payment. This is time consuming since it also depends on the speed of the internet on the ETM as well. Only after the QR Code is generated, can you make the payment. Thus, the total time taken to print the ticket takes close to 10-15 seconds. A downside according to me is that the QR Code appeared as invalid on MobiKwik, forcing me to use GPay. The QR Code must be compatible with all payment apps under NPCI’s BharatQR system.

MTC QR Code displayed on the ETM (Pic: BESTpedia)

Overall, it seems that the NCMC is ahead, but let me share two instances that make it the clear winner.

The first instance. A few weeks back, I was traveling to Bangalore. Now recently I have been getting off at Shanthinagar TTMC (Atal Bihari Vajpayee TTMC ) and taking a bus back home. I usually pay by cash but on this day, I had only a ₹500 note on me. This was the week after I first used UPI to buy a ticket. Unfortunately for me, my phone battery ran out, and for some reason, my phone refused to charge, either from my battery pack or from the USB port on the bus. (The cable was at fault, I bought a new one). Which meant that without a phone, I had to pay in cash, which was also a problem since I didn’t have change. Eventually I managed to make change at a shop inside the terminal, albeit the shopkeeper gave it to me grudgingly.

The second instance is a more recent one. On 12 April, UPI services faced a five-hour long outage. This was the longest in over three years and one of four such outages over a three week span.

Now, both these instances were unprecedented and of course problematic.

So, what could be the solution? Going back to the Card? Maybe. At least with Transit.

UPI was introduced to ensure that transactions were conducted domestically, therefore reducing their costs. But then, NCMC is entirely built atop the RuPay platform which operates domestically, unlike Visa, MasterCard, American Express, or Discover.

This is not to put down UPI however. It is a fantastic platform. However, in cases like public transport, which experiences high volume density of transactions, it makes more sense to use the NCMC.

What are your thoughts? Do let me know in the comments section below.

What comes to your mind when someone says “The World’s ‘smallest’ car?”

Family Guy joke on Giant Samsung Phone being a Tiny Kia Car, hosted on BESTpedia

I’m sure many of you may have different ideas when you hear the word ‘smallest car’ and some of you may have seen the above scene from Family Guy but still.

In fact, there exists a car that is officially adjudged as the world’s smallest car –the Peel P50 – manufactured by the British (Manx, from the Isle of Man) Peel Engineering Company that was famous for its fibreglass boats in the 1950s through the 1970s when it folded.

The Peel P50 (left hand side, in blue) with its successor the Peel Trident (right hand side, in red). Image: Andrew Bone via Flickr/Wikimedia Commons

The Peel P50 was recognised in 2010 by the Guinness Book of World Records as the smallest production car ever made.

Interestingly, the British also made the Welbike, a portable, foldable single-seat motorcycle manufactured by the Excelsior Motor Company of Birmingham under the management of Station IX during World War II. The bike was designed to be folded into the standard CLE Cannister to be airdropped and then be used.

A Welbike inside the Canister at the Army Museum in Paris (Image: Van Der Meulen Christofle/Wikimedia Commons)

Anyway, coming back to the topic of small cars.

The P50, on record remains the smallest car. Now, for those of us who grew up in the early 2000s, we might have seen this on the third episode of the tenth series of Top Gear, hosted by Jeremy Clarkson. Clearly, for Clarkson, the P50 was too big, as evinced by the pilot episode of the nineteenth series, a mere six years later, when he built the P45, an even smaller car, which, from the looks of it was essentially looked like he was wearing an oversized raincoat while driving on a cart through London.

Jeremy Clarkshon driving the P45 (LG62 LYF)

The P45, built by Clarkson, and called the ‘birth of the future’, was compliant with most of the United Kingdom’s regulations relating to motor vehicles. Based on a quadricycle, it featured a 100-cc, two-stroke engine with a 1.7 litre petrol tank, which could be swapped out for a battery-powered motor, thus making it a hybrid, albeit restricting it to a speed of 3 miles/hour with the battery lasting just the hour. It also featured a reverse gear, something the P50 didn’t have.

Clarkson began by driving the P45 (the base model as he called it, with a “premium” feature being a hand-held wiper to clean the alleged windshield) on local roads before getting onto main roads and eventually the A3 road to reach London where he got so scared that he took the car with him on a bus for the rest of the journey. In London, he drove it into a mall, did some shopping, where he ran it on electric mode and then headed to the British Library to check how quiet the electric mode was, before running out of battery. He also drove it to the theatre to watch a show.

Clarkson also pitched the P45 to the investors of Dragon’s Den (what Shark Tank was known as before) where it ostensibly got rejected for being, well “impractical”.

You can watch Jeremy Clarkson’s adventures with the P45 on YouTube too:

Interestingly, Clarkson also has a show on Amazon Prime UK titled Clarkson’s Farm, which is a farming documentary.

What is the smallest car in India?

At the surface level, there are many answers to this question. Older people might answer Maruti 800, some may say Tata Nano or its electric variant, the Jayem Neo. Some might recall Chetan Maini’s Reva or its successor, the Mahindra E2O. A more recent answer is the MG Comet. Some may include quadricycles such as the Bajaj Qute or the Mahindra Atom.

The real answer here is something totally different. Built by Indore-based Wings EV, the Wings Robin is billed as India’s first microcar and is the same length as an average motorbike. It’s a two seater, with one seat behind the other, much like a two-seater aircraft, although the manufacturer claims it can support 2.5 people.

Here’s what the Robin looks like.

The Wings EV Robin during a test run. Photo via Wings EV on Youtube

(Fun fact: This test run was done at Adarsh Palm Retreat in Bangalore. I saw a test run there last month, but by the time I pulled out my phone, the car had sped away)

There are other names floating around too, if you know any, drop a message in the comments below.

It’s been a while since I posted anything Delhi related. The last post, written in the context of the 2016 demonetisation excercise, was critical of the Delhi Transport Corporation’s ethics, especially due to allegations of the body being used to launder money. Read: DTC and Ethics: No connection there

So, here goes. As reported by ThePrint, Delhi’s bus melee has been quite chaotic.

In the decade that started with the financial year of 2011-2012 and ended in 2021-2022, the Delhi Transport Corporation (DTC) inducted just two buses into its fleet. That’s right, just two! The matter came to light when the long-pending Comptroller and Auditor-General (CAG) report was finally tabled by the Government of the National Capital Territory of Delhi (GNCTD) recently.

The DTC’s fleet shrunk from 4,344 in 2015-16 to 3,937 in 2021-22. This was despite the availability of over ₹230 crore for the procurement of new buses. Now, to get some context. A 2007 directive by the Delhi High Court asked for the fleet strength to be increased to 11,000 buses by 2009. It was around this time that the erstwhile Blueline buses were phased out and the Cluster Bus scheme was introduced. The cluster bus scheme, under the Delhi Integrated Multi-Modal Transit System (DIMTS) was to operate 5,500 buses with the balance 5,500 to be operated by the DTC. However, as per the report, on 31 March 2022, only 7,001 buses were operational in Delhi, with 3,762 of them being under DTC and 3,239 being under DIMTS. Concurrently, the DTC’s financial liability soared to ₹65,274.3 crore in 21-22 from ₹28,263 crore in 15-16!

After 2011-2012, only two electric buses were procured by the DTC, that too in March 2022. By that time, the low-floor CNG buses that were operating across the National Capital had exceeded their 12 years of useful life. Of the 3,937 buses in the DTC fleet, 1,770 were overage by March 2023. Only five buses were overage in 2018-19, forming 0.13 per cent of the total fleet and that number rose sharply to form 44.96 per cent of the fleet. Subsequently, the DTC procured a mere 300 electric buses till 2023. Nine proposals had been approved by the Corporation’s board between 2013 and 2021 but none went to the tendering stage because either the GNCTD didn’t give formal approval, or because the GNCTD changed the specifications. There was also an inordinate delay in finalising the bids for the electric buses, resulting in the DTC losing ₹49 crore as assistance from the Central Government under the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme.

Now, the implications of this are pretty clear. DTC’s fleet utlisation remained at 85.27 per cent in the financial year 2021-2022, as opposed to the expected 92 per cent availability for DIMTS contractors. There were between 2.90 and 4.57 breakdowns per 10,000 km due to the exceeding age of the fleet. This was much higher than other transcos and even the DIMTS. In stark contrast to this, the DIMTS fleet saw its fleet utilisation stay at 99.01 per cent during the same period (2021-2022).

It has been a very bad decade for DTC. Clearly. Remember in 2016, there were allegations that the Aam Aadmi Party was using the DTC to launder money in the aftermath of Demonetisation?

In the recent past, one major change in how we commute is how ride-sharing platforms have changed their operations. Prior to the pandemic and lockdown, everything was online, digital and there was a lot of crying around. But now, the system has completely changed.

Let’s start with the most obvious change. You can no longer automatically pay for auto rides in most cities in India. You have to manually pay your driver at the end of the trip and more often than not, things don’t exactly go as per expected.

The story of protests against Uber and Ola over the contentious issue of commissions is not a new one. High commissions from the aggregators’ side have led to multiple instances of violence, with taxis being set on fire, offices and vandalised and even customers being harassed and abused. I’ve been at the receiving end of it myself, in 2017. You can read about it here: Bengaluru’s Uber, Ola Drivers’ Greed Has Led to Hooliganism on The Quint.

Then came Namma Yatri. And along with it, the guilt tripping. “WHY USE AN APP THAT CHARGES THIS MUCH COMMISSION WHEN YOU CAN USE AN APP THAT HAS ZERO COMMISSION?” is the standard argument all their ads have made. Remind me again who was involved in arson and violence? Not the commuter. Who gets guilt-tripped? The commuter. The person who pays for the service.

Now, NammaYatri is backed by JusPay, a payments processor. This is important because as a fintech firm, JusPay knows how much it costs to operate a ride-hailing service.

With aggregators moving away from the earlier model to basically acting as a connecting platform for drivers. In 2016, I had written that India is better off with Uber and Ola drivers being labelled as self-employed. You can read it here: India Is Better Off With Self-Employed Uber And Ola Drivers. In the article, I had argued that the ‘self-employed’ model of drivers was indeed the best model for cabdrivers as it gave them the flexibility to operate, which would be gone if they were to be classified as regular employees. My view has remained the same, albeit my stance on libertarianism has softened significantly, especially post the pandemic and consequent lockdowns. Remember I had once posted about a platform called ‘LibreTaxi’? Move Over Ola and Uber, LibreTaxi Is Here.My views on this have changed significantly.

Now, before I go into the main story, let me also drop another name here: ONDC and the Beckn protocol. The Open Network for Digital Commerce (ONDC) is a Government of India-backed public technology initiative that was launched in 2021 to enable a level playing field for smaller players in the e-commerce field. It was meant to provide an open, inclusive system for retailers, shoppers, technology platforms and prevent cartelisation of the sector by Big Tech giants like Amazon, retail giants like Walmart (through Flipkart), and even our homegrown duopolies of Zomato and Swiggy. Eventually, it has evolved into an ecosystem that today also includes the transport sector (through Namma Yatri).

If you want to see how ONDC functions, simply open the Paytm app, and search for either ONDC Food or ONDC Shopping. You can then place an order directly with the restaurant, who will then dispatch the order via a delivery partner (Dunzo, ShadowFax or others) and you pay with the app itself. ONDC is also available through other apps such as PhonePe, but I’ve only used it on Paytm.

The Beckn protocol functions as the backbone of the ONDC ecosystem by treating each entity (discovery, booking, payment, delivery and fulfillment) as separate entities or micro-transactions. Do read What is the Beckn protocol – the backbone of ONDC? To get a full understanding of how things work. Note. I absolutely love ONDC. It has made things cheaper, especially food deliveries. But while ONDC acts similar to using an aggregator for purchases, ride-sharing is a different story.

Now, coming back to Ola, Uber, Rapido, Namma Yatri, and their new model of services.

For starters, under the old model of operations, there was some accountability. Auto-drivers, especially in Chennai, who have never operated by meter were beginning to get in line. However, in this new method of operation, the idea is ‘please discuss the fare with the driver’, or ‘negotiate the fare with the driver’, which essentially means, pay whatever the driver demands since we are no longer involved and in the event you get overcharged, then you can’t even go and claim a refund.

Rapido in fact tells you that the fare is not enough if nobody accepts the trip and starts nudging you towards increasing the fare. Namma Yatri too does something similar, except it calls it a tip. Ola meanwhile just says your fare will be between x and y, please discuss it with your driver and in my experience, they demand more than what the higher number is. Off-late, Rapido has extended this ‘tech-stortion’ to bikes as well. And on top of that, the captains demand ‘tips’.

Another important aspect is privacy. Yes, while drivers already had access to some data about you, such as your name where you are going and your phone number (kudos to Uber and Namma Yatri for masking my number), now they will also know which bank I use and my legal name.

Alternatively, there is the case where drivers flat out refuse to accept online payments and demand cash because they don’t want to use a bank account (Hint: It has to do with Income Tax). If you’re lucky, the driver won’t argue too much and may not abuse you.

One more important factor is time. With the earlier model of letting the app handle payments, all I had to do is get out of the vehicle and go on my way. With the direct payment model, that is problematic. My phone’s battery might be low, I may not have a stable internet connection, (both of these have happened to me) and the lamest excuse: The driver is waiting for the SMS to reach his phone. When I asked an Uber driver when he got paid (for in-app payments), he told me payments are processed daily, and he got paid at the end of a calendar day. I don’t see what the problem with that is. Most of the users are salaried employees who get their salary at the end of the month.

In the recent past, once this new model of operations became the norm, there have been many cases when autowalas have refused to accept a ride for a certain fare. For the commuter, the app suggests that they either bump up the price or offer an extra tip (depending on the app) in order to get drivers to accept the ride. This is basically going back to the old method of haggling over fare before settling down on what the driver wants.

Ridesharing was meant to bring in order into an otherwise unorderly sector, but it seems to have done the exact opposite. At the same time, governments have begun to look at autos as a perennial vote bank and therefore neither enforce meter rates nor penalise them for overcharging. Essentially, it’s the commuter who is left in the lurch.

What are your views on this? Do drop a note in the comments below.